0

Table of Contents

Four Fintech development trends you should know about

So, what do the next few years post-pandemic have in store for the industry? Here are four fintech development trends and predictions you should keep an eye on!

The fintech industry was already experiencing a slow but steady growth before the pandemic hit. Surprisingly enough, during the COVID-19 lockdowns, the sector saw even more innovation and growth than it had ever experienced before. Some say it has skyrocketed because the transaction value increased amidst numerous lockdowns, and digital services became the only worthy alternative.

So, what do these next few post-pandemic years have in store for the industry? Will the financial technology sector continue to advance? Here are four fintech development trends and predictions you should definitely keep an eye on!

A boom in digital-only banking

The rise of digital-only banks or “neo-banks” is a hot development in the fintech industry that can completely transform how the world does banking. In contrast to traditional banks, neo-banks don’t have physical branches and are operated fully online or via smartphone-based apps. This is why many digital banks collaborate with a fintech design agency - to produce apps and websites with user and mobile-friendly design principles.

It’s also no secret that digital banks are on a growth trajectory and will likely become much more common in the next few years due to the recent shift in consumer habits after the pandemic. According to the latest data, 64.6% of people with a bank account used online banking in 2021, and this number is predicted to grow exponentially in the coming years.

This rise in popularity of digital banking is primarily because it offers underbanked populations a convenient way to make deposits and other types of financial operations. It also eliminates the need to visit brick-and-mortar branches, saves you from long queues, and removes the hassle of filling out tedious paper-based forms.

If you’re planning to finally take advantage of this boom that’s still going strong and launch a mobile banking app, be sure to check out our posts on the benefits of good UX design in fintech and why design is key to building trust in this industry.

Growing acceptance of blockchain technology

Anyone who has paid attention to the fintech space in the last few years knows blockchain technology's potential to revolutionize how this industry operates. It became one of the most significant innovations for digital transactions because of its philosophy of decentralized finance, which means its management gets distributed without being under the control of a specific company, individual, bank, or government.

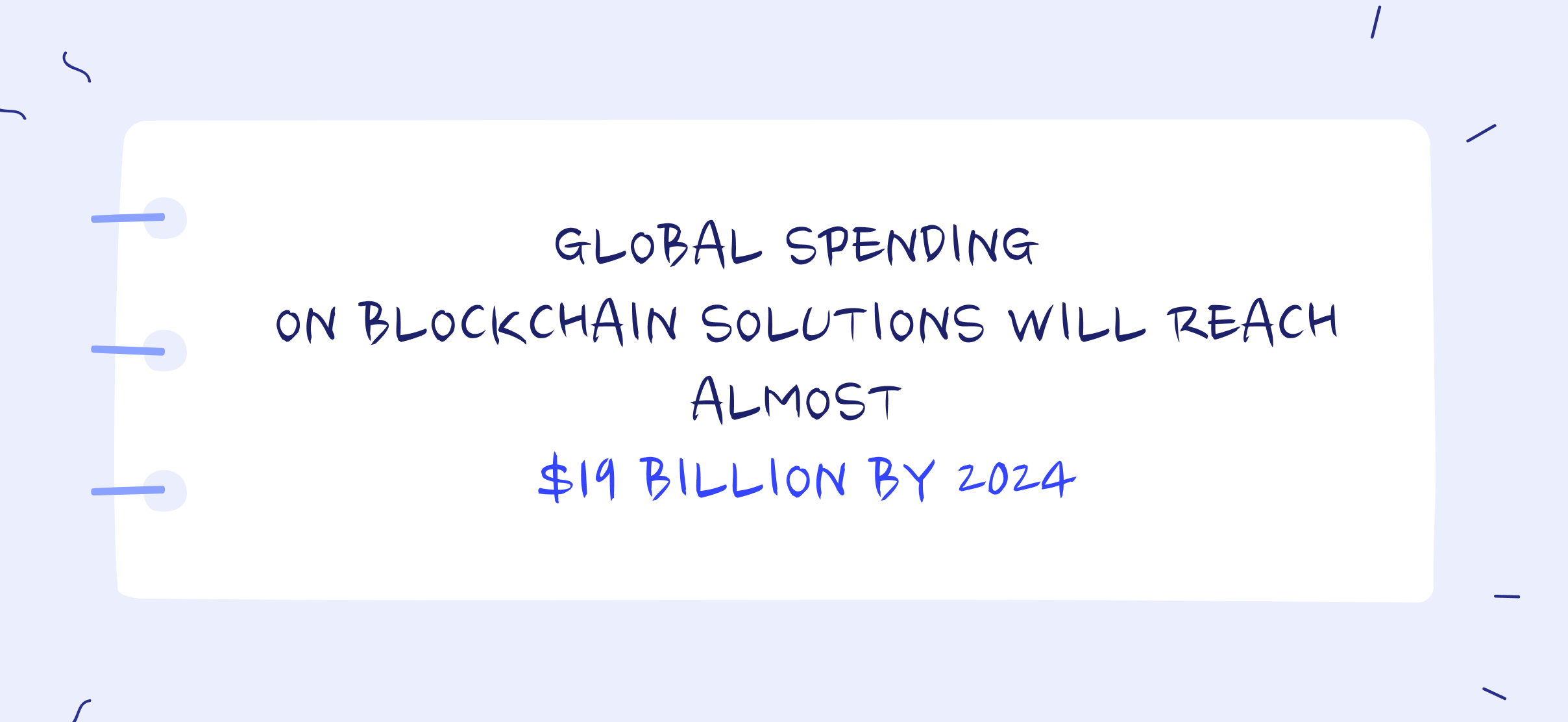

Although some people are still concerned about the legality of blockchain-powered transactions, the growing acceptance and popularity of blockchain as a means to create a secure digital ledger is something that can't be ignored. As of now, the global spending on blockchain solutions is around $6.6 billion, and forecasts suggest it will reach almost $19 billion by 2024.

A rise in embedded finance

Embedded finance is a term that describes the integration of financial services into non-financial platforms. A good example is a cab booking app that includes built-in payment solutions.

Embedded finance has been gaining popularity over the last few years. And it is now poised to grow at an even higher rate as several banks are set on becoming service providers to non-financial and non-bank institutions, seeking to deliver a better customer experience or value proposition involving financial services as a part of a bigger offering.

A vital part of embedded finance is the buy-now-pay-later service, which is on track to become mainstream in the next few years. Smart solutions like Klarna and PayPal already offer consumers precisely what they desire when shopping online — seamless and easy-to-execute transactions.

Incorporation of robotic process automation (RPA)

As the name suggests, RPA uses digital programs, software, and robots to automate repetitive and routine activities previously performed by humans.

RPA technology differs from artificial intelligence (AI) because it doesn’t require human-like processing power and is commonly used for simple back-office tasks like information processing and data entry.

Many businesses in the fintech industry have already started to adopt RPA technology to lower costs, free up resources, and boost overall business efficiency.

Perhaps the biggest benefit of RPA is that it increases productivity at a relatively small investment without sacrificing quality. This allows businesses to focus on major areas like customer service and other value-adding and innovative activities.

Currently, this technological innovation is valued at $3.17 billion and is predicted to grow to more than $13 billion by the year 2030.

What’s next for Fintech?

We can safely say that the rise of non-traditional banking is not over. The neo-banks we mentioned at the beginning of this article have already turned into a staple in Fintech rather than a hot new trend. Banking will become even more open to consumers, giving them a more comprehensive picture of their personal finances and how to manage them.

And last but not least, safety in the digital banking sector will become even more pronounced due to all the latest regulations and changes that will ensue. Customer protection is the number one priority, and accountability will rise even more to give people that desired peace of mind when it comes to trusting their personal financial information.