0

Table of Contents

9 customer experience banking mistakes that kill your retention (and quick fixes)

Today’s customers compare their experiences not just to other banks, but to the best user experiences they encounter anywhere.

Customer loyalty in banking can vanish overnight if you get the experience wrong.

Did you know that poor banking customer experience is directly responsible for banks losing up to 20% of their customers?

The worst offenders range from confusing apps and slow service to impersonal “one-size-fits-all” approaches. These mistakes frustrate users and drive them into the arms of fintech competitors.

What to do?

Tackle these issues head-on with better design and a customer-first mindset.

In this guide, we’ll break down nine deadly mistakes in digital banking experience that secretly kill user retention, and show how to quickly fix each one.

By the end, you’ll know exactly how to deliver the best banking experience that keeps customers happy and loyal.

What is customer experience in banking?

Customer experience in banking (often called banking CX or banking user experience) encompasses every interaction a user has with a bank’s products, services, and channels.

It’s the entire journey from the first contact to achieving a financial goal. This includes the ease of navigation, accessibility, security, mobile banking features, customer support, and even branch or call-center interactions.

In simple terms, if someone asks, “What is banking experience exactly?”, it’s the overall feeling and satisfaction a customer gets from using a bank’s services across all touchpoints.

A positive banking experience means the user finds it easy, fast, and safe to manage their finances, whereas a negative experience means they feel frustrated, confused, or underserved.

The modern digital banking experience is heavily influenced by user-centric tech companies. Customers now expect banking to be as seamless as hailing a ride or ordering food on an app.

That’s why banking customer experience is how you win users.

Customer expectations from banks

Today’s customers have high expectations for their banking experience. With many alternatives just a tap away, meeting these expectations is critical for retention.

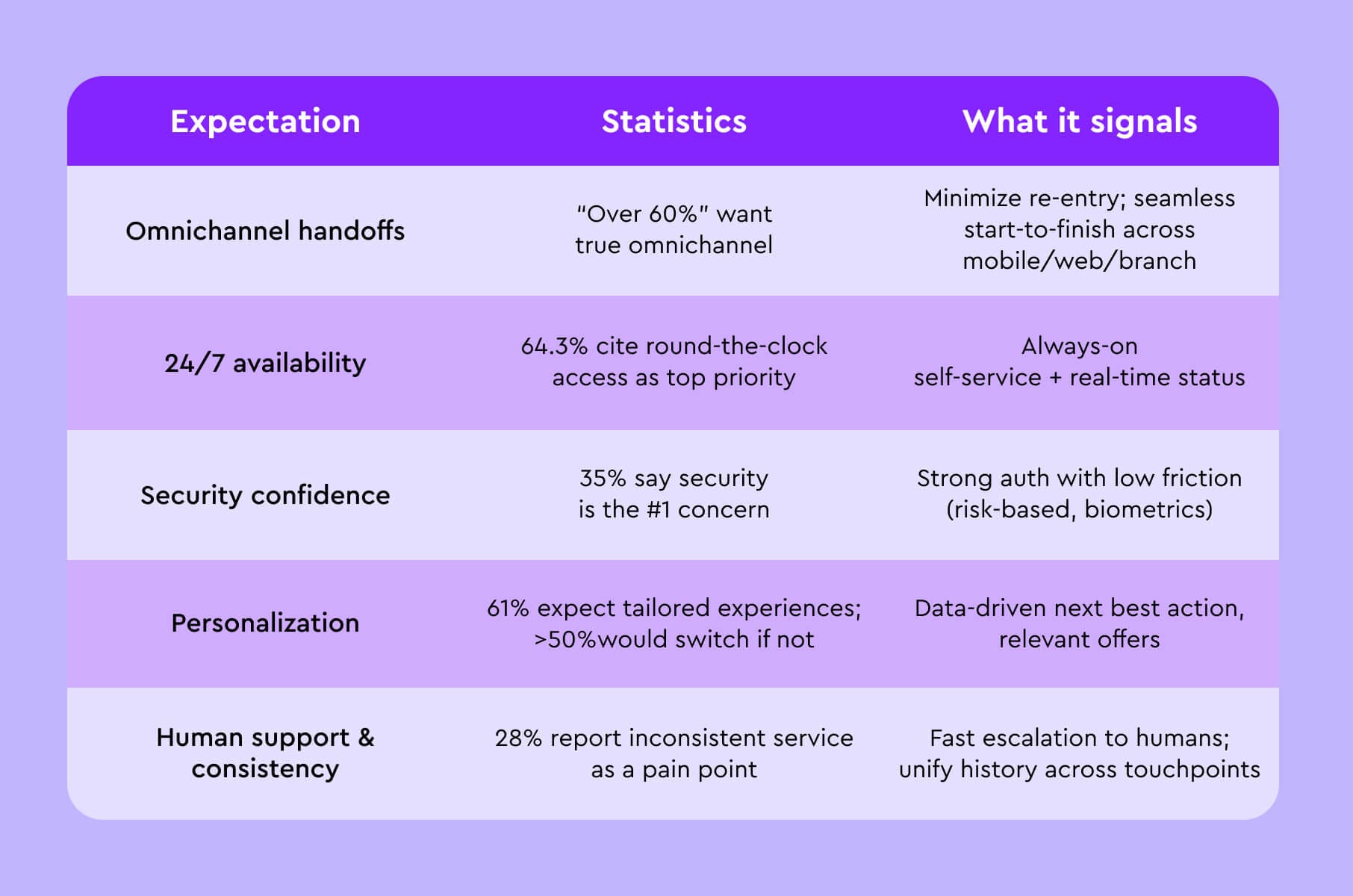

In the table below are some core customer expectations from banks in the digital age:

And a breakdown:

- Customers want to start a process on one channel and finish on another. They hate having to repeat information or deal with disconnected systems. Over 60% of consumers say they want a true omnichannel banking experience with smooth handoffs between mobile, web, and branch.

- Banking should be fast, 24/7, and accessible. In a survey, 64.3% of people said 24/7 access to accounts is a top priority.

- Security is the №1 concern about online banking for 35% of people. They expect robust security measures but with minimal inconvenience.

- 61% of banking customers expect companies to understand their unique needs. More than 50% would switch providers if services weren’t personalized, showing how vital this is to a good banking customer experience.

- Despite the shift to digital, customers still want empathetic human support for complex issues. They expect chatbots and FAQs for simple queries, but also an easy way to reach a real person when needed. Roughly 28% of consumers cite inconsistent customer service as a pain point in banking CX.

If you fall short on any of the above, you risk delivering a subpar customer experience banks cannot afford – and your users might quietly slip away to a competitor who does better.

Customer experience trends in banking

Before we go any further into banking customer experience mistakes, let’s briefly go over current customer experience trends in banking:

From AI-driven chatbots to proactive insights on spending, the goal is to make the digital banking customer experience feel custom-fit for each user. For example, predictive algorithms can now suggest budget tips or recommend products at just the right time, mimicking the personal touch of a human advisor.

- “Phygital” integration

Leading banks blend digital and physical experiences. Customers might get an app notification about a pre-approved loan and then have a seamless in-branch visit to finalize it. Banks are breaking down silos so that whether a customer is on a smartphone, laptop, or at a branch, the banking experience is consistent and connected.

Onboarding is becoming faster with innovations like biometric ID verification, digital KYC, and instant account opening. The trend is to remove paperwork and face-to-face requirements, allowing users to join entirely from their device. Banks know first impressions matter, so they’re investing in onboarding flows that feel almost effortless.

Staying aware of these trends helps in improving the customer experience in banking. Fintech startups often set the pace here, with agile experimentation, while incumbents are catching up by adopting similar tech and customer-centric design practices.

How to improve customer experience in banking

Every bank, especially fintech startups building from scratch, should ask: How do we improve customer experience in banking to keep users engaged and loyal?

The answer lies in continuous, user-focused improvement. Here are some proven strategies for improving the customer experience in banking:

- Shift from a product-centric approach to a customer-centric one.

- Audit every user journey (sign-up, fund transfer, card application) for unnecessary steps.

- Invest in modern, responsive design. Looks and usability matter.

- Regularly update your design system to meet evolving user expectations (dark mode, biometric logins, voice commands, etc.).

- Use the data you have to make the experience feel personal.

- Focus on performance optimization (fast load times, smooth transactions) and clearly communicate security measures.

Partnering with experienced fintech design teams can often accelerate these improvements.

For instance, our team at Merge specializes in fintech design and development services (see our fintech design & development page) to help craft user-centric banking products.

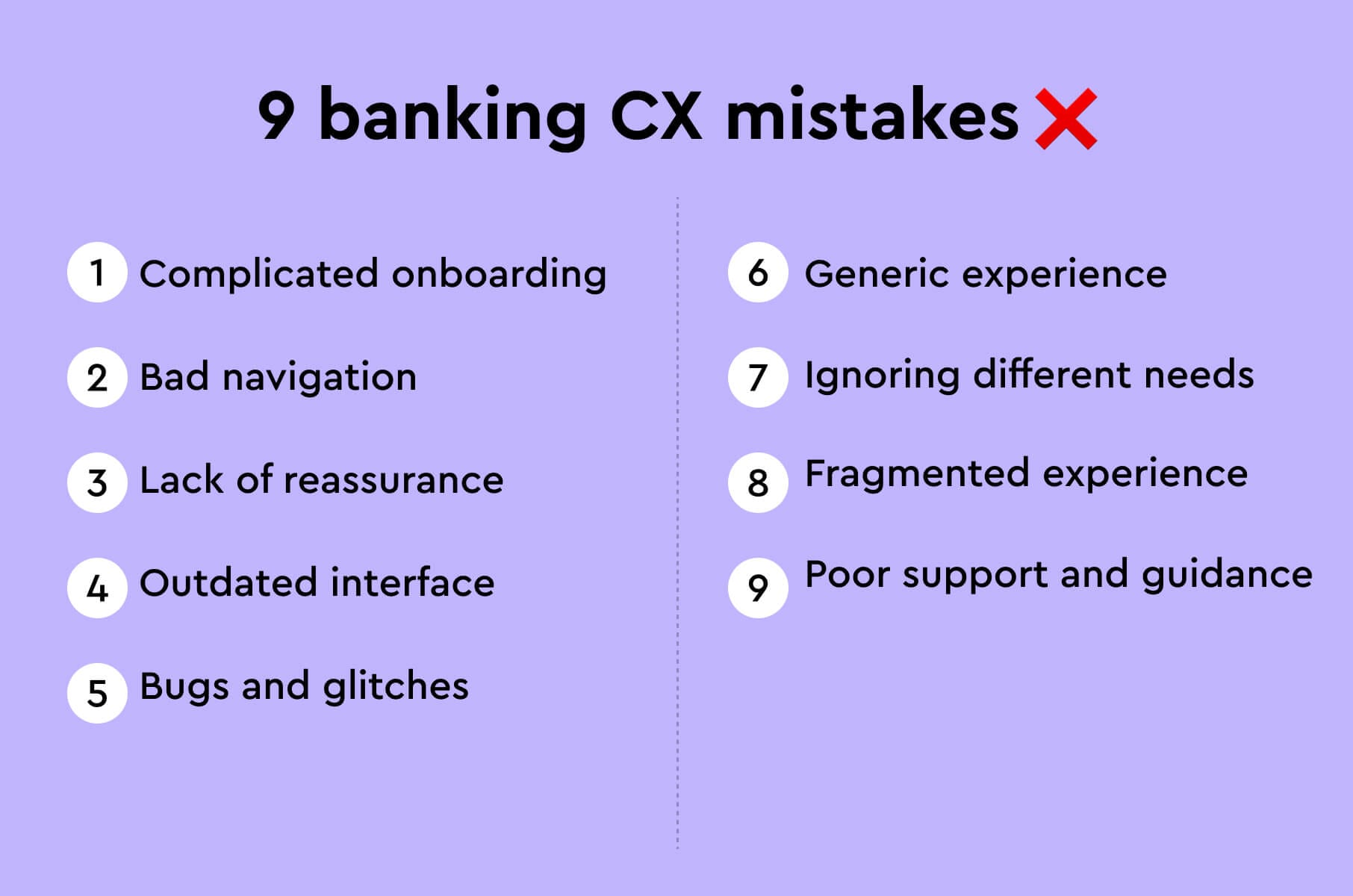

9 banking customer experience mistakes (and how to fix them)

For each mistake, we’ll see why it hurts retention and how to fix it quickly to deliver a standout banking customer experience.

1. Complicated onboarding

How it kills retention:

If a user never completes onboarding, they obviously won’t stick around.

But even those who struggle through a clunky onboarding may start their relationship with your app on a sour note. It sets the tone that using this service will be a pain.

That first-session churn is deadly.

These users often won’t return, meaning all your marketing spend to acquire them is wasted. One bad onboarding experience can lose a customer forever.

Quick fix:

Simplify and streamline onboarding with user experience in mind. Ask only for essential information upfront. You can always collect secondary details later once trust is established.

- Implement modern solutions like biometric login or scanning IDs to reduce manual data entry.

- Provide a progress indicator and the option to save progress and resume later (so a missing document doesn’t cause a total restart).

- Also, consider a guided onboarding with tooltips or a friendly checklist so users know what to expect next.

For example, one fintech client of ours had a 5-screen signup with dense forms. We redesigned it into a two-step process with clear progress markers and added an option to skip non-critical steps initially. The result was a significant drop in abandonment and a smoother start for users.

The key is frictionless entry.

Get users to their “aha!” moment (like seeing their account dashboard or a successful first transaction) as quickly as possible.

2. Bad navigation

How it kills retention:

A common banking UX mistake is cramming too much into the interface or using confusing menus and labels.

Confusion leads to frustration, which leads to abandonment. If routine tasks (checking balance, transferring money, paying a bill) turn into a scavenger hunt, even loyal users will use your app less.

They might revert to using your competitor’s app or even going back to branch banking out of frustration. Over time, your active user counts drop, and churn rises.

Confusing navigation essentially makes your service feel unreliable and not user-friendly, eroding the overall digital banking customer experience and sending people away.

Quick fix:

Redesign your information architecture with a “don’t make me think” approach. Conduct usability tests or card-sorting exercises to see how real users expect to find key functions.

Often, the fix is to simplify menus and use clear, user-centric labels.

Some tips:

- Instead of ambiguous terms (“Products” or “Your Journey”), use straightforward labels like “Accounts”, “Payments”, “Investments”, etc.

- Prioritize the most common tasks on the home screen or navigation bar.

- Include a search bar or smart shortcuts for power users to jump straight to what they need.

3. Lack of reassurance

How it kills retention:

The moment a user feels their trust in the platform drop, they are likely to go away.

For example, if your app glitches during a funds transfer and the user isn’t sure it went through, that anxiety can make them afraid to use it again. They might revert to going to a branch or using a competitor they perceive as safer.

Trust issues often manifest as users avoiding high-value features – like they might check their balance on your app, but hesitate to set up a large transfer or deposit because they’re not confident it will work correctly. Eventually, low trust can push customers to close accounts.

Quick fix:

Add trust cues into your banking customer experience design. Some quick wins:

- Display a padlock or “secure” icon in the login screen and in the URL on web.

- Show reassuring copy like “Protected by 128-bit encryption” or “[Bank] will never share your data” in FAQs or during sensitive actions.

- Use consistent, professional design – audit your app for any element that looks broken or out of place (even a typo can reduce credibility).

- Ensure error messages are clear but not alarming. If something fails, say “We’re having trouble, but your data is safe – please try again” rather than a scary tech error.

- Provide easy access to support: a visible help button or live chat gives users confidence that if an issue arises, they can get assistance.

4. Outdated interface

How it kills retention:

Today’s users, especially millennials and Gen Z, compare your app’s design to the slick experiences of fintechs and big tech.

You might not get direct complaints that “the app looks ugly,” but you will see the effects in user behavior.

Outdated design often correlates with poor usability too (e.g., not optimized for new phone screen sizes, no dark mode, etc.), which frustrates users.

We’ve observed cases where banks with dated apps see lower adoption of new features – not because the features aren’t useful, but because the presentation doesn’t entice users to try them.

Quick fix:

Check current UI/UX best practices!

Key areas to address: responsiveness, contemporary color palette and typography, features that users have come to expect (dark mode, biometric login, and customizable dashboards).

Even subtle updates like fresh icons and smoother animations can make the app feel new.

If you have the resources, consider developing a design system that standardizes the UI components. As a quick win, identify any element that users have commented “feels outdated” and refresh that first.

Sometimes, partnering with a specialized fintech design team (like ours at Merge) is helpful to inject modern design trends while respecting your brand.

5. Bugs and glitches

How it kills retention:

If your mobile banking app takes too long to load, lags when displaying account info, or frequently shows error messages, it’s doing serious harm to the digital banking experience.

Repeated slowdowns create a perception that using your service is a hassle.

Users might keep their account but use it less frequently, or they’ll maintain a secondary account with a competitor and eventually shift their primary activities there.

Worse, if a technical glitch causes something like a duplicate charge or a false balance display, trust is broken (tying back to mistake №3).

Quick fix:

Performance tuning must be a top priority as part of UX. Start by measuring: use analytics to see where drop-offs happen.

Once you have targets, optimize ruthlessly: compress images and files, remove redundant network calls, and use loading skeletons or progress bars to give feedback during any wait. Aim for that magic under-3-second load for main screens.

Also, test under real-world conditions. Not just on high-speed Wi-Fi in the office, but on a typical mobile network with average device specs.

If something does go wrong, communicate it – a simple in-app message “Sorry, services are slow right now, we’re on it” is better than leaving users guessing.

6. Generic experience

How it kills retention:

A generic digital banking experience might mean the app shows the same promotions or tips to everyone (offering a student loan ad to a retiree – irrelevant), has no customization options (can’t reorder accounts or hide features one doesn’t use), and never surfaces insights from the user’s own data.

All of this leads to a lack of engagement.

Users will only use the app for basic necessities (like checking balance or simple transfers) and ignore the rest. This means you miss out on cross-selling opportunities, and the user doesn’t develop a deeper relationship with your platform.

61% of banking customers expect companies to understand their needs, and more than half will switch if they don’t get personalized service.

Quick fix:

Start introducing personalization and customization features into your banking customer experience. This doesn’t require creepy levels of data use – even simple things go a long way. For example:

- Give users the ability to customize their dashboard: let them rearrange widgets, nickname their accounts, or choose what summary info they see first.

- Greet your user by name and highlight their most-used features.

- Use segmentation to show relevant content.

- Automatically categorize the user’s expenses.

Ultimately, improve customer experience banking platforms by treating each customer as an individual. It can start small, but even minor personalization features can boost user satisfaction.

7. Ignoring different needs

How it kills retention:

An often overlooked aspect of digital banking customer experience is accessibility.

If your app or website isn’t usable by people with disabilities or differing needs (visual, auditory, cognitive, motor), you’re effectively turning away a segment of potential users and possibly violating regulations.

Quick fix:

Conduct an accessibility audit of your app/website – many tools and consultants can identify issues like contrast problems, missing alt-tags, or navigation that’s impossible via keyboard (for those who can’t use a mouse or touchscreen).

Simple fixes:

- Use high-contrast colors for text and important elements.

- Provide a toggle for larger text sizes in-app if possible.

- Make all images/icons have descriptive labels for screen readers.

- If forms and workflows that are usable via keyboard alone (which also indicates good screen reader compatibility).

Also, consider different contexts: does your mobile banking app work with voice assistants or have voice command options for users who can’t easily type? Some banks have started adding basic voice control for banking actions.

8. Fragmented experience

How it kills retention:

Customers interact with their bank through multiple channels – mobile app, website, branch, ATM, call center, maybe even chatbots or messaging apps. One of the biggest customer experience banking mistakes is treating these channels as separate silos rather than one continuous journey.

According to research, having to repeat information across touchpoints remains one of the top customer service hassles. And 60% of consumers want to be able to switch seamlessly between physical and digital channels during a single interaction.

Quick fix:

Work towards a unified omnichannel banking experience. This involves technological integration and process changes, but some quick fixes are possible.

For instance, implement a universal CRM or case tracking for customer support so that if a customer contacts you on chat and then on the phone, the agent can see the context.

Customers should be able to pick up where they left off as well: if they save an application online, a branch employee should be able to retrieve it.

A true story: one bank we know integrated their ATM, app, and branch systems so that if an ATM failed to dispense cash, the user got a push notification to their app with an apology and info on the failed transaction, and the branch staff could see it too.

Customers were pleasantly surprised that they didn’t have to do anything to report the issue.

9. Poor support and guidance

How it kills retention:

28% of consumers cite inconsistent customer service as a challenge in banking.

Even with the best-designed app, users will occasionally have questions or issues. Maybe a transaction didn’t go through, they need to dispute a charge, or they simply can’t figure out how to use a feature. If at that moment your bank makes it hard to get help, you’ve created a frustrating dead-end in the banking user experience.

Customer service is part of the customer experience, not separate from it, so it must be top-notch.

Also, customer support interactions are often crucial moments, and a well-handled issue can actually increase loyalty.

Quick fix:

First, ensure your app and website have a clear Help or Contact Us section – ideally with multiple channels (FAQ, chatbot, live chat, phone callback request, community forum, etc.). Modern customers often prefer not to call, so live chat or in-app messaging is a great option – but only if it’s actually helpful.

Invest in a knowledge base so that whether customers self-serve or ask an agent, the answers are consistent.

During design, integrate support touchpoints contextually – e.g., a (?) icon on complex forms that explains jargon or an option to chat if a form error keeps happening.

People remember how you made them feel at critical moments. Make them feel heard, helped, and valued.

How to measure customer experience in banks

Unlike pure numbers like revenue, customer experience is a bit more complex, so you should rather track a combination of qualitative and quantitative metrics. Here are some key ways banks measure CX:

- Net Promoter Score (NPS)

“How likely are you to recommend our bank to a friend or colleague?” on a 0-10 scale.

A high NPS means users are happy and likely to stay (and promote you); a low NPS signals issues in experience that could be driving people away.

- Customer satisfaction (CSAT) and effort scores (CES)

“Rate your satisfaction with our mobile app today,” or “Was it easy to accomplish your task?”

After key interactions (like a support call, a loan application process, or an app transaction), ask customers to rate their satisfaction or how easy the process was.

- Retention and churn rates

Track what percentage of customers leave (close accounts) vs. stay, and how this correlates with their engagement.

Also monitor digital drop-off rates (like how many start onboarding vs. complete it, how many initiate a feature vs. finish it). A high abandonment in a user flow indicates a CX problem there.

- Usage analytics and adoption rates

Which features are people using frequently, and which are hardly touched?

Track active users (DAU/MAU), session lengths, and event funnels for critical journeys (like steps to make a transfer).

A smooth digital banking experience should show healthy engagement.

- Customer complaints and support data

Analyze your support tickets, call transcripts, and chatbot logs. What issues come up most? How quickly are they resolved?

A rise in complaints about, say, mobile check deposit failures or confusing statements pinpoints an experience issue. Also, track first contact resolution rate (resolving issues on first touch).

We’ve noticed that banks that rigorously track CX metrics and act on them are the ones that consistently deliver the best banking experience in the market.

Winning at banking customer experience

Great customer experience banking is a continuous commitment to better understanding and serving your users.

Remember that today’s banking customers compare their experiences not just to other banks, but to the best user experiences they encounter anywhere (Uber, Amazon, Apple, etc.). It’s a high bar, but by avoiding these nine mistakes, you’re well on your way to meeting it.

Focus on delivering convenience, trust, personalization, and support at every touchpoint.

When in doubt, put yourself in your customer’s shoes: would you enjoy using your bank’s app or service? If not, go back to the drawing board – and consider enlisting expert help if needed.

At Merge, for example, we’ve helped many fintech products refine their UX and UI, ensuring that the customer is always front and center.

A friendly reminder: if you need fintech design and development expertise to boost your bank’s CX, our Merge team is one click away.