0

Table of Contents

Gen AI in banking: 11 mind-blowing use cases you can launch now

Gen AI is generative and draft‑based. What can it do in banking? Let's find out.

Quick answer for busy banking leaders – these are the 11 generative AI use cases in banking we’d launch first, because they are proven, compliant by design, and deliver measurable ROI:

- KYC and AML case‑copilot that drafts investigation summaries and SAR narratives with audit trails.

- Credit underwriting memo generator that turns raw financials and PDFs into analyst‑grade credit write‑ups.

- Frontline banker copilot embedded in CRM that cites policy and produces next‑best‑actions with reasons.

- Gen‑AI dispute assistant for Reg E and chargebacks that guides reason codes, letters, and merchant evidence.

- Contact‑center “first‑90‑seconds” summarizer with real‑time guidance and escalation notes.

- Collections coach that proposes hardship plans and generates compliant follow‑ups.

- Marketing micro‑experience generator that spins compliant landing copy and disclosures for each segment.

- Fraud intel summarizer that links cases, merchants, devices, and entities into human‑readable briefs.

- Policy and controls Q&A with retrieval‑augmented answers and citations to internal policy.

- Developer copilot for regulated codebases with secure RAG, pattern snippets, and guardrails.

- Synthetic data workbench for privacy‑preserving test datasets and red‑team scenarios.

Now, if you are not in a rush, scroll down for a breakdown of each and lots more helpful information on Gen AI in banking.

What is general AI in banking?

General AI in banking refers to predictive and decisioning systems that classify, rank, forecast, or recommend based on structured data, while Gen AI (Generative AI) in banking refers to large‑model systems that generate text, code, or images and can reason over unstructured data to produce drafts, answers, and actions.

What is the difference between general AI and gen AI?

Difference: general AI is discriminative and score‑based. Gen AI is generative and draft‑based. Both belong in one operating model, but they solve different steps in a workflow:

- General AI in banking includes scoring models for credit, fraud, marketing propensity, and risk. They are narrow, supervised, and optimized for numeric outputs.

- Gen AI in banking. Those are systems that generate text, code, or images based on context. They excel at document‑heavy and knowledge‑heavy work such as memos, emails, customer assistance, and policy Q&A.

- If it's a product design implication, our advice is to combine them. Use general AI to decide and GenAI to explain and communicate the decision with sources and policy citations.

11 generative AI banking use cases you can launch now

Here’s an execution‑ready set of workflows that can pay back really quickly.

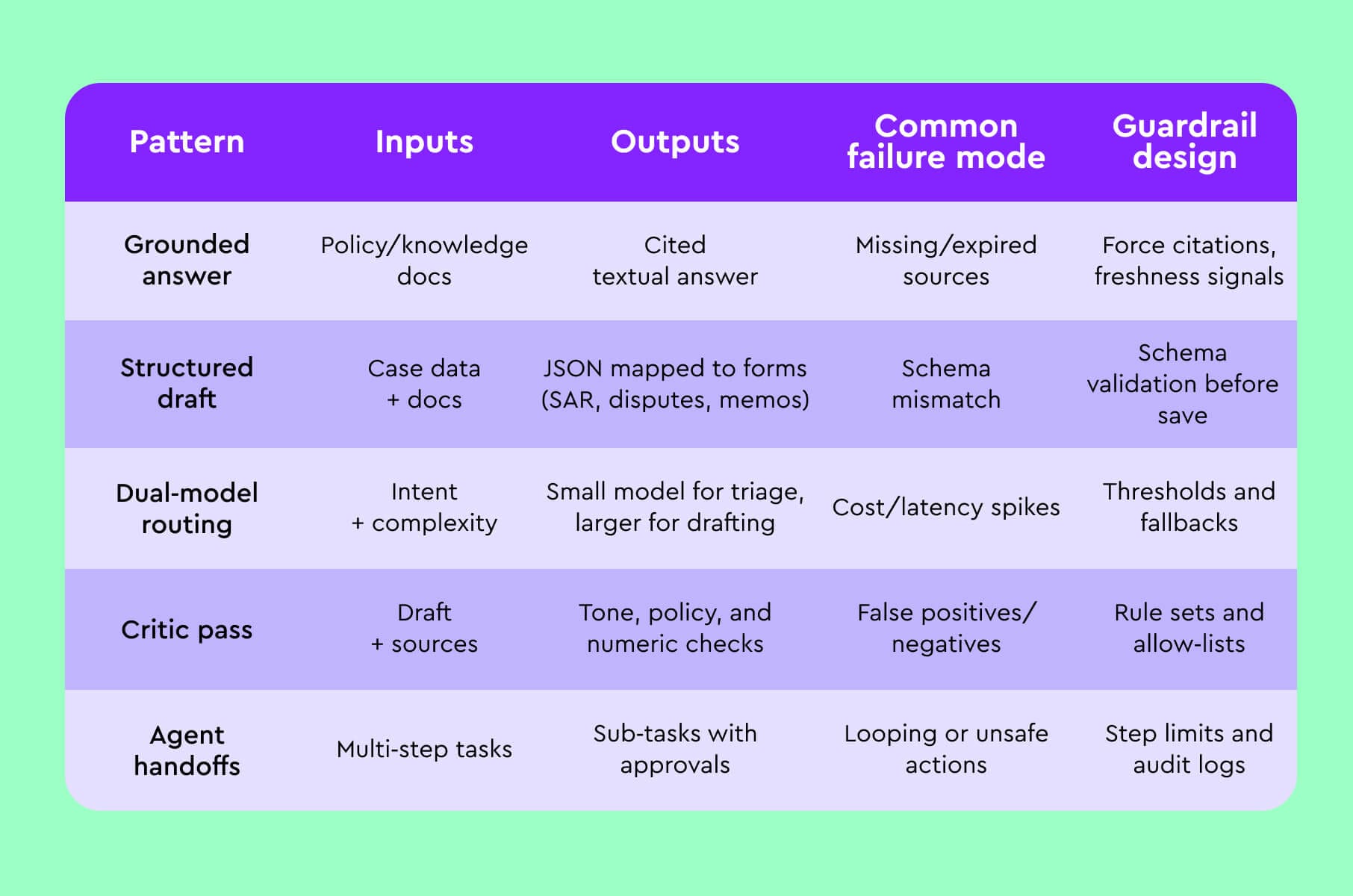

1) KYC and AML investigation copilot

This is where Gen AI in banking shows its value in messy, document‑heavy work.

Issue to fix or process to improve:

Would you like an analyst’s drafting bench that never sleeps?

What to build:

A case side‑panel that pulls transactions, watchlist hits, and adverse media, then drafts a SAR narrative the analyst can edit. Use retrieval‑augmented generation (RAG) over your case store and a policy‑grounding index that knows your filing standards.

How it works:

The copilot ingests alerts, case notes, adverse media, and transaction graphs, then proposes a SAR narrative with clear sections – suspicion summary, timeline, counterparties, and supporting evidence. It highlights unusual flow patterns in plain language and links every claim to a line in the ledger or an alert ID. Analysts accept, edit, or reject each block, and the system logs those decisions for audit.

2) Credit underwriting memo generator

Among generative AI banking use cases, this one protects quality while compressing cycle time.

Issue to fix or process to improve:

It so happens that underwriting is very slow because facts hide inside PDFs, emails, and bank statements.

What to build:

Parse borrower PDFs, bank statements, and financial spreads, normalize into a ledger, then generate a credit memo with covenants, cash‑flow commentary, and sector comps. Add a fact‑check pass that reconciles generated assertions to line‑item math before surfacing to an analyst.

How it works:

The memo generator normalizes documents into a structured ledger, computes cash‑flow diagnostics, and drafts a credit view. It also proposes covenants, flags thin coverage, and compares peer metrics that your policy allows. A fact‑check pass reconciles every number to its source before a human signs off.

3) Frontline banker copilot inside CRM

This next one is a practical generative AI for banking example that raises advisor capacity without confusing compliance.

Issue to fix or process to improve:

Advisors miss context because it lives across call notes, emails, and policy pages.

What to build:

A sidebar that reads call notes, emails, portfolio events, and policy, then proposes next-best actions and drafts compliant follow‑ups, all saved to Salesforce or Dynamics.

How it works:

A CRM‑embedded copilot displays a one‑screen brief – household changes, recent service pain, portfolio drift, and relevant offers – then drafts a follow‑up email that cites policy language when needed. It never answers from memory, only from the bank’s knowledge base and transaction history the advisor is allowed to see.

4) Gen‑AI dispute assistant for Reg E and chargebacks

Among generative AI use cases in banking, this one is an easy early win because the work is template‑driven and measured to the minute.

Issue to fix or process to improve:

Disputes involve strict timelines and picky documentation.

What to build:

Guided flows that detect reason codes, assemble evidence, draft customer letters, and produce merchant packages, with timers for regulatory deadlines.

How it works:

The assistant guides agents through reason codes, auto‑collects device and merchant evidence, and drafts letters that match regulatory templates. It also proposes the next action – provisional credit, merchant outreach, or escalation – with reasons shown on the screen. When paired with simple automation, banks cut manual touches per case and reduce write‑offs from misclassified claims.

5) Contact‑center copilot

And this one is generative AI in banking tuned for the front line, not a chatbot trying to replace agents.

Issue to fix or process to improve:

Every second counts when a call starts.

What to build:

Real‑time transcript, instant customer history summary, and dynamic guidance for secure authentication and offers.

How it works:

The copilot reads the transcript in real time, pulls authenticated context, and presents a compact brief – identity checks, recent complaints, likely intent, and recommended next step. It suggests phrasing that avoids promises the bank cannot keep and shows policy citations for edge cases.

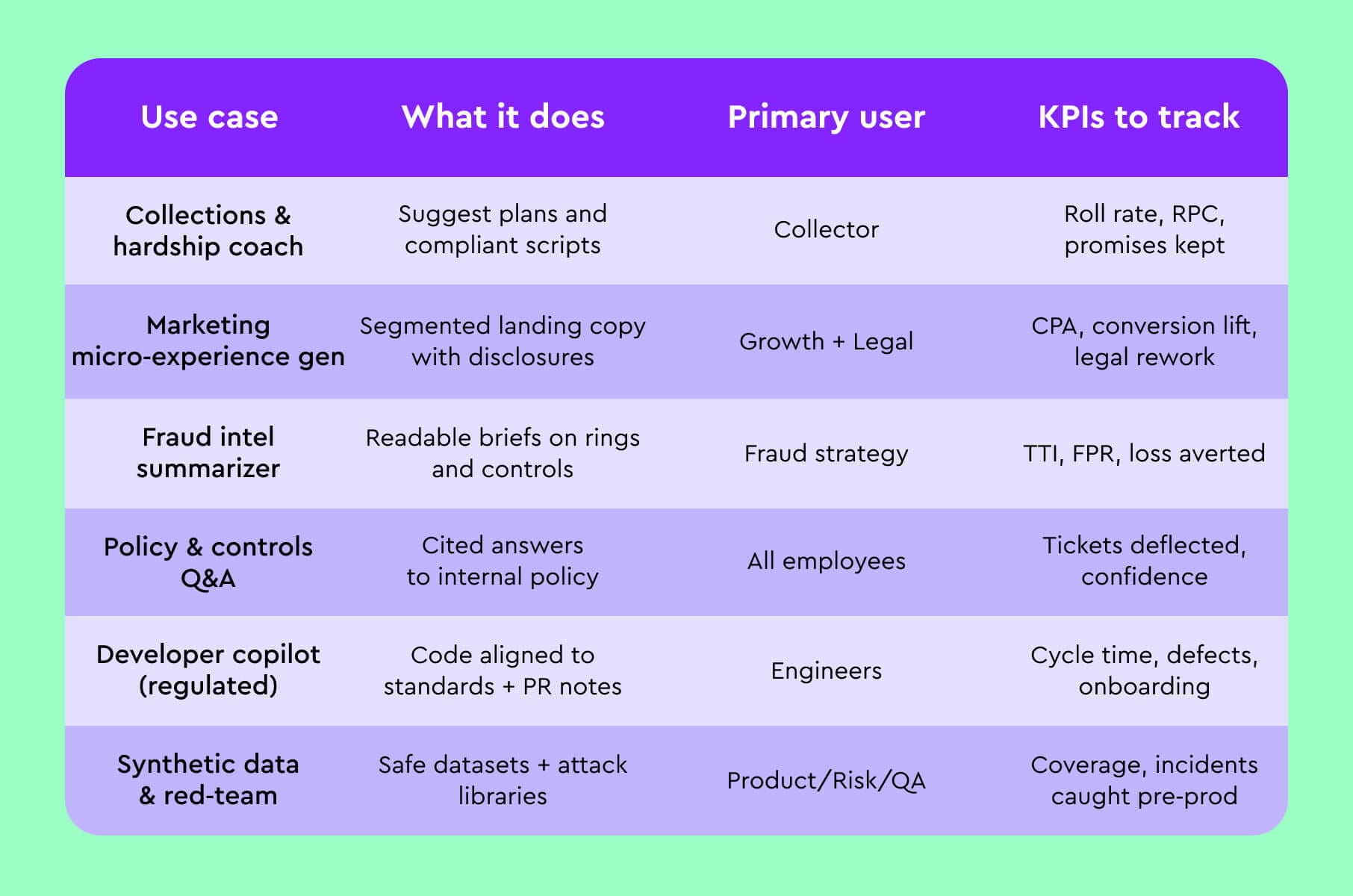

6) Collections and hardship coach

Now, here's one of the use cases of AI in banking that directly reduces losses.

Issue to fix or process to improve:

Collections teams need empathy and structure at the same time.

What to build:

Call guidance that proposes tailored hardship plans, drafts compliant follow‑ups, and books callbacks.

How it works:

The coach suggests a hardship plan based on account behavior, income shocks, and policy‑approved options, then drafts a compliant follow‑up message that sets expectations and due dates. It warns agents when phrasing could be construed as unfair or misleading and logs the approved script for audit. The system also reminds agents when a promise‑to‑pay is due and proposes the next nudge.

7) Marketing micro‑experience generator

Among generative AI banking tools, this one is a multiplier for overworked marketing and legal teams.

Issue to fix or process to improve:

Modern growth teams do not want a thousand random tests. They want a handful of precise micro‑experiences per segment that already include the right disclosures.

What to build:

A component that creates 1‑to‑few landing copy, subject lines, and in‑app nudges per segment with auto‑disclosures and legal references.

How it works:

This generator turns a positioning brief into landing copy, push copy, and in‑app banners, all cross‑checked against your legal library. It can suggest two distinct narratives – value‑seeker and convenience‑first – and automatically pair them with matching imagery and CTA length recommendations.

8) Fraud intel summarizer for risk teams

This is generative AI banking used as an analyst multiplier rather than a black‑box decision engine.

Issue to fix or process to improve:

Fraud teams often stare at link charts that only analysts can parse.

What to build:

A tool that pulls device, merchant, account, and network signals to summarize fraud rings and propose controls. Include graph‑aware retrieval so the model “speaks” in entities and links.

How it works:

The summarizer explains the pattern in clear text (how devices, merchants, and accounts connect) and calls out the controls the bank should tune. It proposes a rule experiment, predicts the false‑positive impact, and drafts a briefing for product and operations so changes can go live without confusion.

9) Policy and controls Q&A for employees

This is one of the generative AI use cases in banking applied to internal quality, not just customer service.

Issue to fix or process to improve:

Employees ask the same policy questions every day, and email threads are slow.

What to build:

A policy assistant that answers “Can I…” questions with citations to internal policy and decision trees. Great for new hires and branches.

How it works:

A policy assistant answers with citations to the bank’s policy wiki, standards, and approved examples. It never invents rules because answers must contain links to exact paragraphs. The UI encourages safe behavior – a clear “copy with citation” button and a visible policy version number.

10) Developer co-pilot for regulated codebases

For generative AI in banking, this one is a safe, measurable way to free engineering capacity.

Issue to fix or process to improve:

Regulated engineering is all about patterns – auth, logging, encryption, and graceful failure.

What to build:

A private code assistant with RAG over your code and standards, pattern snippets for auth, logging, and encryption, and auto‑PR explanations.

How it works:

The private copilot knows your patterns and generates code that already aligns with them. It writes pull‑request descriptions that explain risks, suggests unit tests for edge cases, and links to the control framework that auditors care about.

11) Synthetic data and red‑team workbench

As generative AI banking expands, this workbench becomes the training ground where you de‑risk features before real customers ever see them.

Issue to fix or process to improve:

Product teams need realistic data without risking privacy.

What to build:

A governance‑approved synthetic data studio to create test datasets for fraud, onboarding, and chat, plus prompt‑injection and jailbreak suites.

How it works:

The workbench generates bank‑grade synthetic datasets for onboarding, fraud, and chat while keeping statistical properties intact. It includes attack libraries – prompt injection, prompt leaking, and social‑engineering scripts – that your agents must withstand before a release.

Some real examples

A few credible implementations that de‑risk your business case:

- NatWest Cora+ is moving from rules chat to generative AI across more complex queries and then expanding via a formal OpenAI collaboration.

- Wells Fargo “Fargo” scaled generative AI to hundreds of millions of interactions without exposing PII to the LLM. Architectural choices like model‑agnostic middleware and data isolation are noteworthy.

- HSBC has credit analysis write‑ups and agent chat summaries to cut process time.

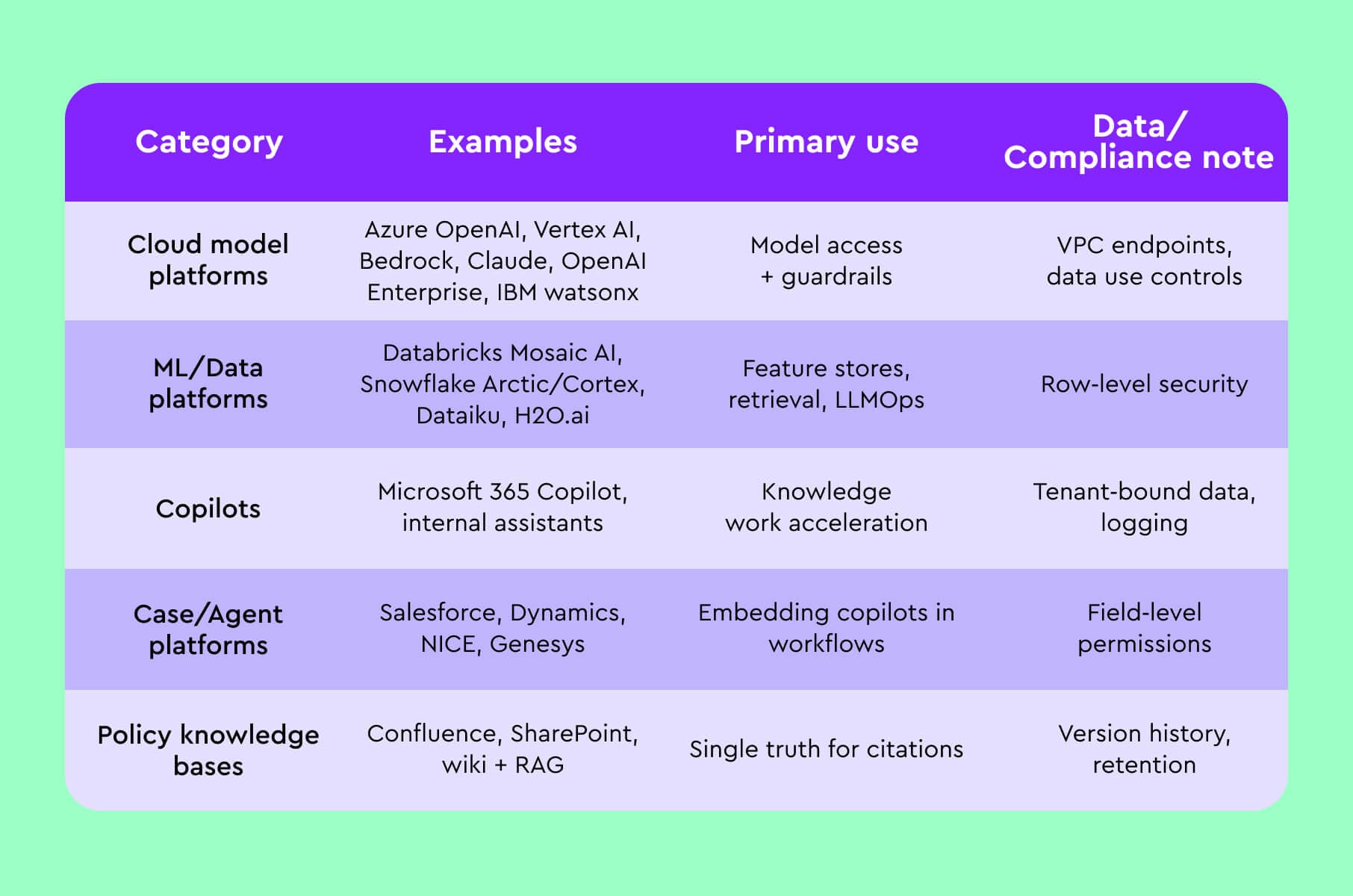

What AI tools are banks using?

Here’s the list to help procurement and architecture narrow choices:

- Cloud model platforms: Azure OpenAI Service, Google Vertex AI, AWS Bedrock, Anthropic Claude, OpenAI Enterprise, IBM WatsonX.

- ML & data platforms: Databricks Mosaic AI, Snowflake Arctic & Cortex, Dataiku, H2O.ai.

- Copilots: Microsoft 365 Copilot at scale across banks like Barclays with a Colleague AI Agent.

- In‑house assistants: DBS‑GPT and SC GPT across dozens of markets.

How is JP Morgan using Generative AI?

Speaking of JP Morgan, here’s how they are using Gen AI. They ought to know something, right?

Internal chatbots and research assistants are live. Back in 2024, JPMorgan launched an in‑house chatbot as an AI‑based research analyst.

Productivity impact

The bank cites 10–20 percent boosts in engineer efficiency from AI coding assistants and is tracking ~450 production use cases with plans for growth.

Client advisory

Executives say AI helped boost sales to wealthy clients during volatility and speed responses, with targeted growth ambitions in the next three to five years.

Strategic signal

Leadership continues to discuss multi‑billion‑dollar AI investments spanning fraud, marketing, service, and research.

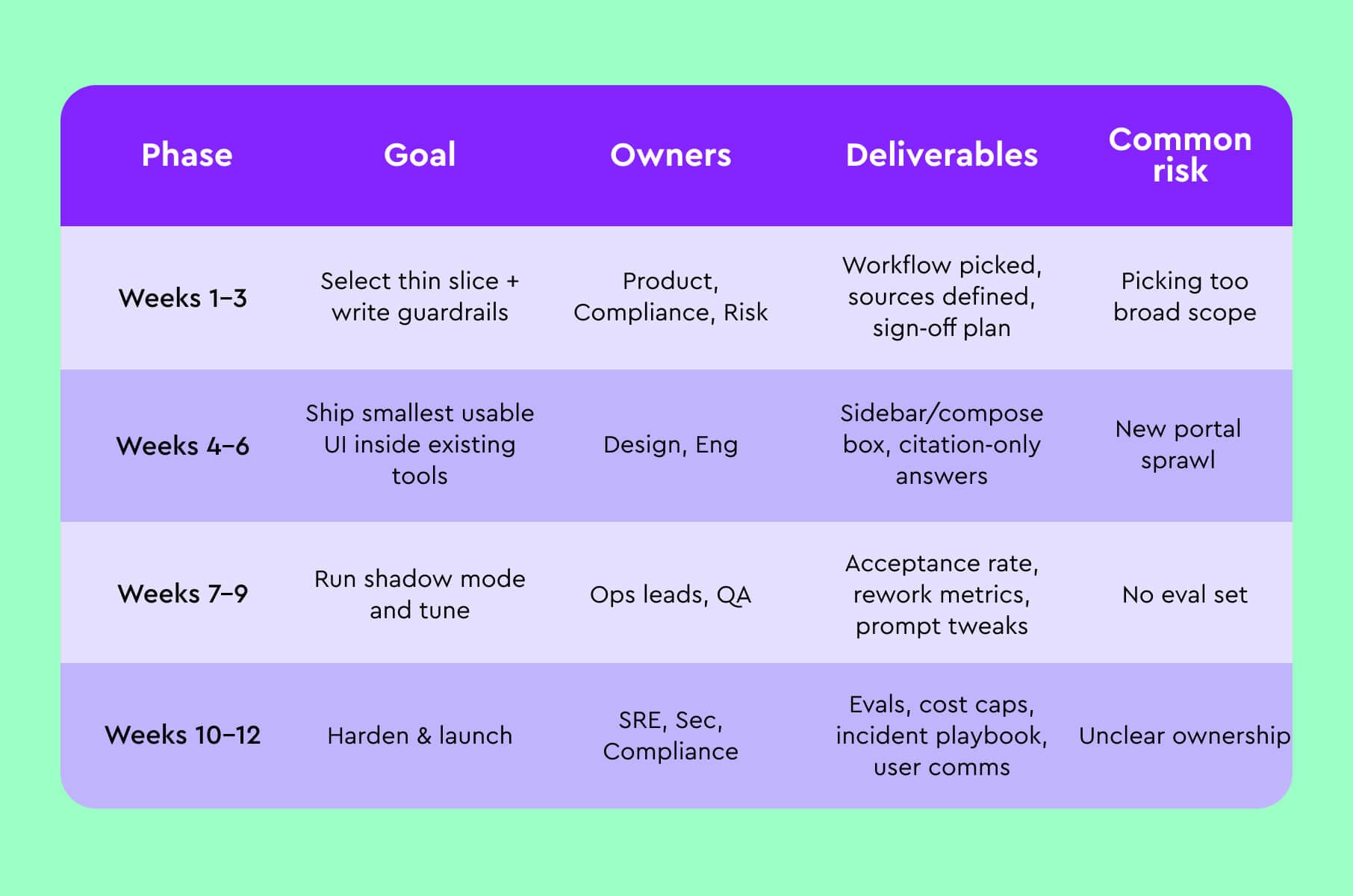

How do you use AI in banking? A 90‑day blueprint

We devised a quick three‑month plan that works when it focuses on one critical workflow.

Weeks 1–3 – pick the flow and write the rules. Choose a workflow with human review by default – SAR narrative drafts, dispute letters, or advisor follow‑ups. Lock the guardrails first – redaction, retrieval sources, critique checks, and human sign‑off.

Weeks 4–6 – build the smallest usable UI. Ship a sidebar or compose box inside the tool people already use, not a new portal. Require citations in every answer and block any response without a source.

Weeks 7–9 – run shadow mode. Compare AI drafts to human outputs, track acceptance rate and rework, then tune prompts and retrieval.

Weeks 10–12 – harden for scale. Add offline eval sets, cost caps, and incident playbooks. Tell staff exactly when they are interacting with AI. If you need a partner, Merge can co‑design and deliver this lane with your compliance team.

What is a limitation of AI in banking?

Most failures are about context, controls, and incentives.

- Hallucinations and over‑confidence if answers are not source‑grounded.

- Disinformation risk: research indicates AI‑generated rumors can move deposits, pressing banks to monitor social media signals.

- Fraud escalation: regulators warn GenAI is already used for synthetic identities and takeover scripts.

- Latency and cost for long‑context tasks without smart retrieval.

- The biggest limitation is organizational. If teams cannot own prompts, evals, and policy mappings like code, progress stalls.

Fix the process, then the model.

What is the future of AI in banking, 2025 edition?

A few AI in banking trends, so you can plan for near-term shifts in next year’s roadmap.

Agentic workflows

Banks pilot multi‑step agents for research and operations. Citi’s report frames the shift to agents that act with less prompting, which matches what we see in bank RFPs.

Enterprise copilots will become normal

Widespread deployments of Microsoft 365 Copilot and internal assistants will move from pilot to BAU, especially for service and ops teams.

More hard governance

The EU AI Act deadlines force banks to classify and document high‑risk use, especially anything tied to credit decisioning or biometric ID.

What is the future of gen AI in banking beyond 2025?

And a few longer‑range signals that guide platform bets:

- Customer‑safe autonomy: limited‑scope agents that can complete back‑office tasks end‑to‑end with human‑in‑the‑loop sign‑off.

- Multimodal by default: voice, screen, and document context handled together for branch and contact‑center workflows.

- Policy‑as‑code: control layers that turn policies into executable checks, gating any generated response.

- AI defense is part of fraud: detection stacks use generative models to simulate attacks and tune defenses continuously.

Helpful internal reads from Merge to plan your rollout

- Fintech UX best practices for designing finance apps – how to present risk and money clearly.

- Best practices for designing AI tools – practical guidance for humane AI.

- The AI development process – a comprehensive guide – what to expect in delivery.

- Creating custom AI solutions for your business – when to go custom vs API.

- Integrating AI into web development workflows – patterns we reuse in portals.

- Fintech dashboard design, or how to make data look pretty – readable analytics for risk and ops.

- Do this, not that: 15 fintech app design do’s & don’ts – UI shortcuts that reduce errors.

- Top AI design tools for UX/UI designers in 2025 – useful for your internal design team.

- 10 best strategies for banking app UX – a compact playbook.

- AI in Fintech. What we know so far in 2024 – context and trends.

Practical takeaways to implement this week

Start with human‑reviewed drafts, such as narratives, memos, notes, and emails. GenAI saves time without making final decisions.

Next - ground everything. No raw model answers. Always retrieve policy and case facts, then generate with citations.

Track business KPIs, not model metrics – minutes saved, rework rate, loss averted, cycle time.

Need a partner to design, validate, and launch your first three generative AI use cases in banking within a quarter?

We can help.

Visit AI development at Merge and Fintech design & development for more details.

Short FAQs

What is Gen AI in banking?

Gen AI in banking is the use of large generative models to create compliant drafts, answers, and actions across knowledge‑heavy banking workflows such as KYC investigations, credit memos, customer service, disputes, and internal policy Q&A.

What is generative AI for banking good at that older AI is not?

Reading and summarizing long documents, explaining outcomes to customers or auditors, and generating structured drafts that map to regulated forms.

What are the most valuable generative AI banking use cases?

The 11 above, especially AML/KYC copilot, credit memo generation, dispute assistant, and advisor/copilot embedded in CRM.

Are there credible examples?

Yes – DBS assistants for contact‑center efficiency, NatWest Cora+ with OpenAI collaboration, Morgan Stanley advisor tools, HSBC credit write‑ups, and JPMorgan coding assistants at scale.